The economy is the backbone that determines the functioning of the world and affects the daily life of every individual. This requires a deep understanding of it.

While there are many different ways of understanding the “economy,” it is essentially the area where goods are produced, consumed, and traded. The economy is discussed at the national level, with experts and journalists often referring to the economies of countries such as the United States, China, and others. However, we can look at economic activity from a global perspective by looking at the activities and jobs of individual countries.

In this article, let's explore more deeply with FUNDGO the concepts related to the economy, based on the model of Ray Dalio, one of the most influential figures in the world of finance.

Who makes the economy?

Let's start with the economy on a small scale first. Every day, we contribute to the economy by buying (i.e. food and household goods) and selling (i.e. working for a paycheck).

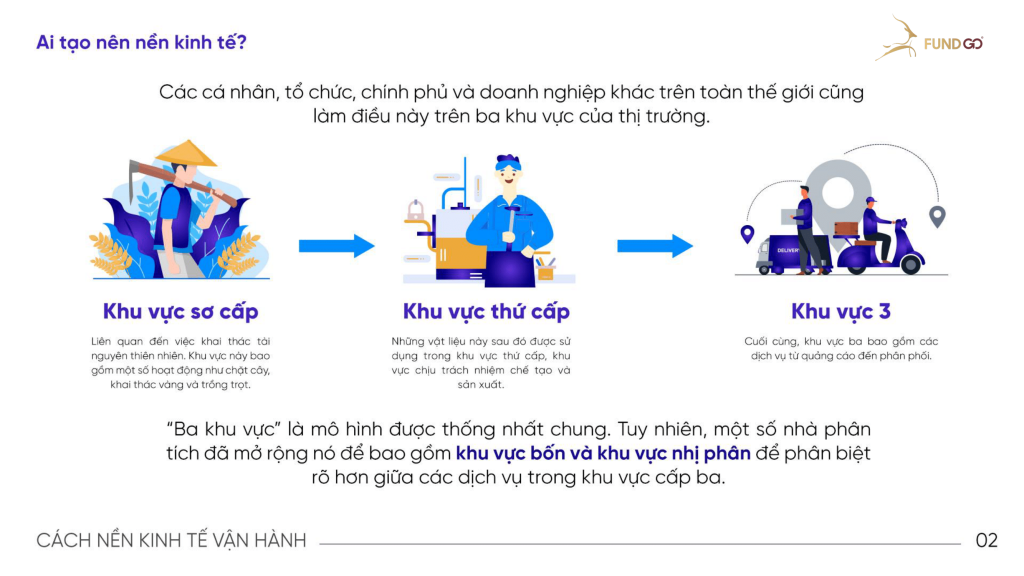

Individuals, organizations, governments and other businesses around the world also do this across three areas of the market.

Primary area: Relating to the extraction of natural resources. This sector includes activities such as logging, gold mining, and farming.

Secondary area: These materials are then used in the secondary sector, the sector responsible for manufacturing and production.

Area 3: Finally, the tertiary sector includes services ranging from advertising to distribution.

The “three sectors” model is generally agreed upon. However, some analysts have expanded it to include a quaternary sector and a binary sector to better differentiate between services within the tertiary sector.

Measuring economic activity

To determine the health of an economy, we can measure it in some way. By far the most common way to do this is to use GDP, or Gross Domestic Product. This measures the total value of goods and services produced in a country over a given period of time.

GDP growth means increased production, income, and spending.

GDP decline shows decline in production, income, spending

Note – Real GDP takes inflation into account, while nominal GDP does not. – GDP is still only an approximate figure, but it is important in national and international analyses. – GDP is a reliable indicator of a country's economy, but it should be cross-referenced with other data to get a more comprehensive understanding.

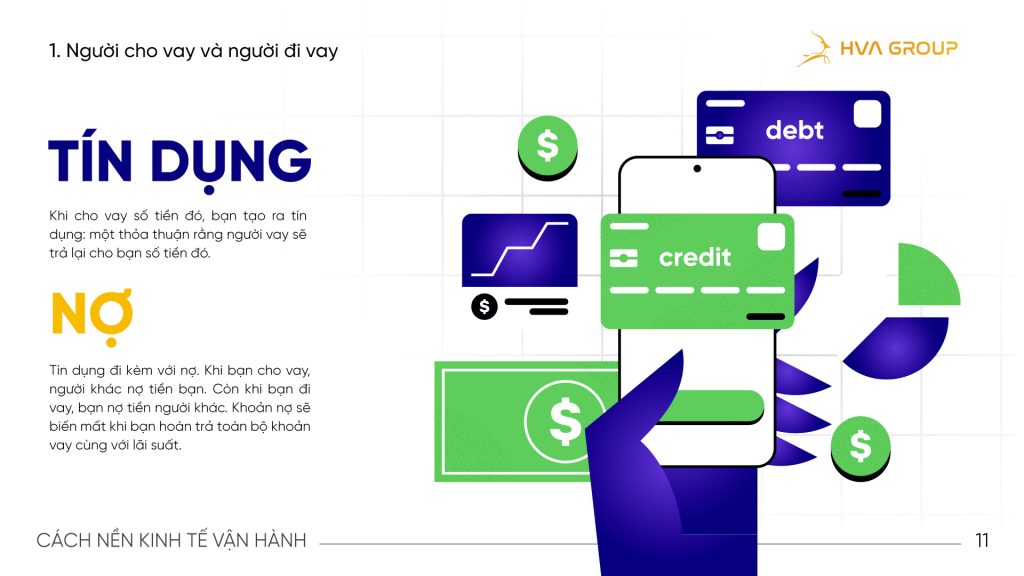

Credit, debt and interest

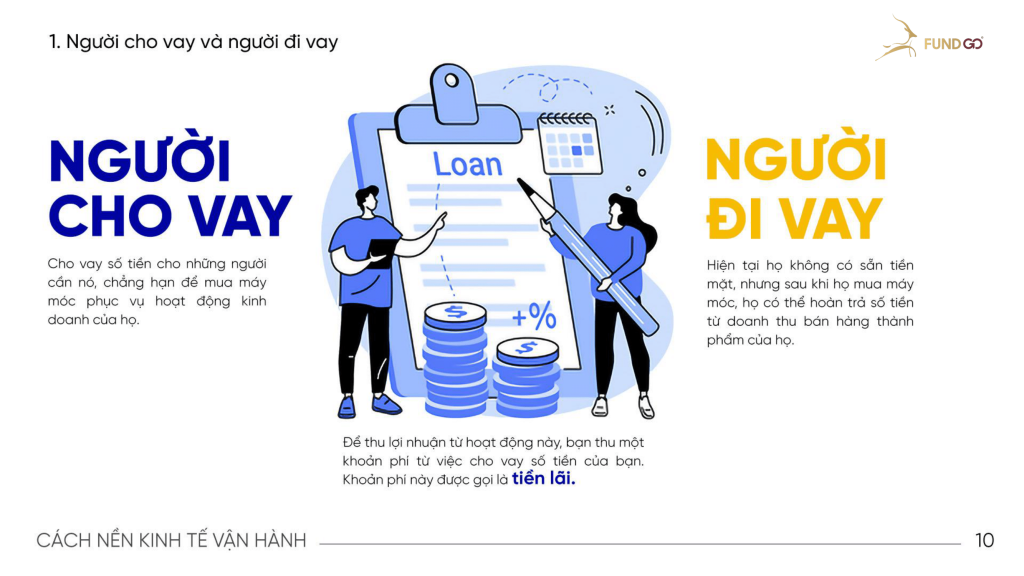

Lenders and Borrowers

Lender: Lend money to people who need it, for example to buy machinery for their business.

Borrower: They don't have cash available at the moment, but after they purchase the machinery, they can repay the amount from the sales of their finished goods.

To make a profit from this activity, you charge a fee for lending your money. This fee is called interest.

Credit: When you lend that money, you create credit: an agreement that the borrower will pay you back that money.

Debt: Credit comes with debt. When you lend money, someone owes you money. When you borrow money, you owe someone money. The debt disappears when you repay the loan in full, plus interest.

Banks and interest rates

Banks: are middlemen (or brokers) between lenders and borrowers. These financial institutions actually play both roles. When you deposit money in a bank, you lend the bank money, and they have to pay you back. Many other people do the same. And when banks have a large amount of cash, they lend it out.

Interest Rates: Banks often encourage you to lend them your money by offering interest rates. Higher interest rates are more attractive to lenders.

Why is credit important?

Credit can be thought of as a kind of lubricant for the economy. It allows individuals, businesses, and governments to spend money that they do not have immediately available.

Banks lend money to high income earners => More access to cash and credit => People spend more money => More people receive income

Some economists say this is not positive, but many believe that increased spending is a sign of a strong economy.

If people spend more, more people will have higher incomes. Banks tend to lend money to people with higher incomes, which means people have access to more cash and credit. With more cash and credit, people can spend more, which creates income for more people, and the cycle continues.

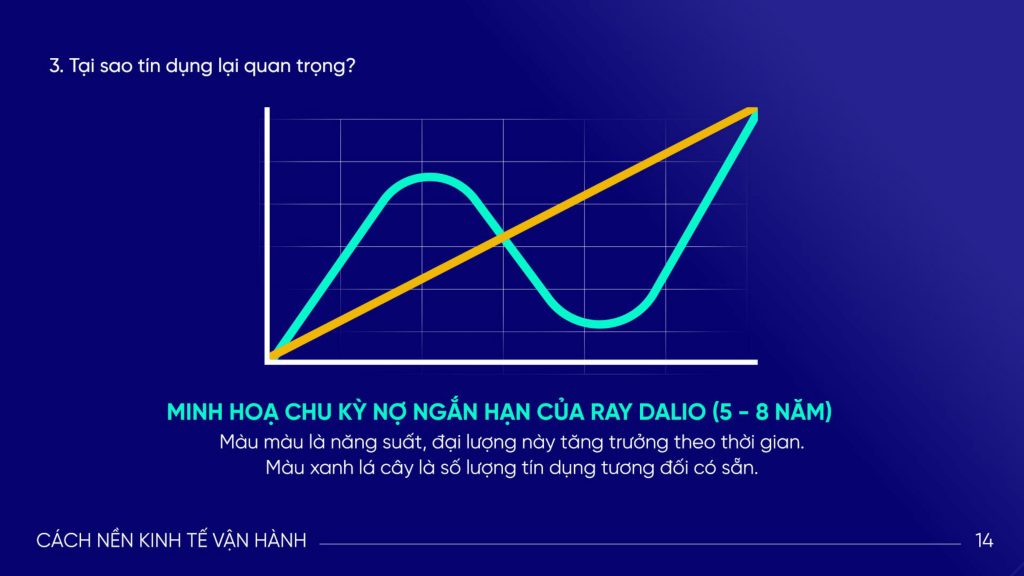

Of course, this cycle cannot continue indefinitely. Ray Dalio has described this concept as the short-term debt cycle, illustrated below. He estimates that these patterns repeat every 5-8 years.

Central banks, inflation and deflation

Assuming everyone has access to a lot of credit, they can buy more than they would without it. However, although spending is increasing rapidly, production is not increasing accordingly. In fact, the supply of goods and services does not increase materially, but the demand does.

Next, this leads toinflation: is when you start to see prices of goods and services rise due to higher demand. A common indicator to measure inflation isConsumer Price Index (CPI), which tracks the prices of common consumer goods and services over time.

INFLATION: The supply of goods and services does not increase physically, but the demand for them does. This is when the prices of goods and services increase due to higher demand.

DEFENSE: Deflation is the opposite of inflation. Deflation is a general decrease in prices over a period of time, usually due to a decrease in spending. Because consumers spend less, deflation can accompany a recession.

How does a central bank work?

Central banks are government agencies responsible for managing a country's monetary policy. Central banks include financial institutions such as the United States Federal Reserve, the Bank of England, the Bank of Japan, and the People's Bank of China.

The central bank's prominent functions are to add money to circulation (through quantitative easing) and to control interest rates. Central banks may raise interest rates when inflation gets out of control. In an ideal world, higher interest rates cause prices to fall due to less demand. But in reality, it can also cause deflation. Deflation can be a problem in certain contexts.

As you might guess, deflation is the opposite of inflation. We define deflation as a general decrease in prices over a period of time, usually due to a decrease in spending. When consumers spend less, deflation can accompany an economic recession. Similar to inflation, deflation can also be measured through the Consumer Price Index.

One proposed solution to deflation is to lower interest rates. When interest rates are lowered, people are encouraged to borrow more. With more credit available, the government expects that economic participants will increase their spending.

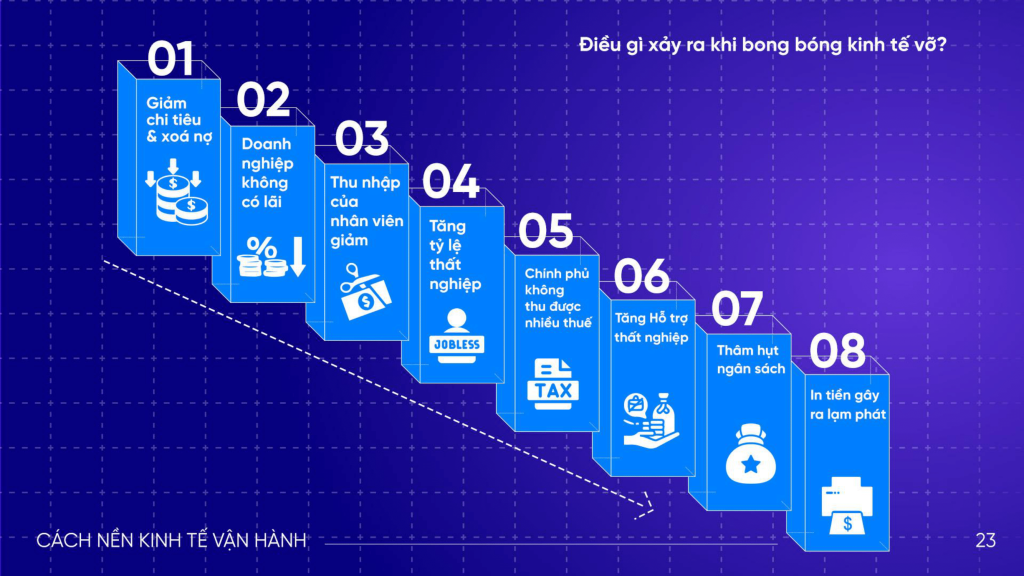

What happens when the economic bubble bursts?

Short-term Debt Cycle: Dalio explains that the chart we illustrate below (the short-term debt cycle) is a small cycle within the long-term debt cycle.

DEBT WILL INCREASE AT THE END OF THE CYCLE: debt becomes unmanageable, causing large-scale write-offs (as individuals attempt to reduce their debt). As the write-offs occur, incomes begin to fall and credit dries up. When debt cannot be repaid, individuals look to sell their assets. But when too many people do this at once, asset prices fall due to the abundance of supply.

01 – Spending control & debt relief 02 – Unprofitable business 03 – Employee income decreases 04 – Increased unemployment rate 05 – The government does not collect much tax 06 – Increase Unemployment Support 07 – Budget Deficit 08 – Printing money causes inflation

When compared to short-term cycles, long-term debt cycles take place over a much longer time frame, believed to occur every 50 to 75 years.

How does all this tie together? Interest rates greatly influence the behavior of people participating in the economy. When interest rates are high, saving makes more sense, since spending is not as much of a priority. When interest rates are low, spending seems to be a more rational decision.

Summary

The economic machine is so large that it can be difficult to understand all of its components. However, by looking closely, we can see similar patterns repeating themselves as participants transact with each other. By now, hopefully you have a better understanding of the relationship between lenders and borrowers, the importance of credit and debt, and the steps central banks take to try to mitigate economic disaster.

Hope with the sharing thatFUNDGO provides you with useful knowledge that helps you gain a deeper understanding of how the economy works. By taking a comprehensive and thorough look at how the economy operates, we can better understand the risks and opportunities and make smarter decisions in managing personal and business finances.

In the early stages of an undemarcated market, the advantage usually lies with the fastest mover. But once the rules of the game begin to be established, market logic changes completely. The advantage no longer belongs to the fastest runner, but to those who can build the infrastructure and control the risks.

Not only through speculation, the multi-million dollar assets of Vietnamese entrepreneurs in the digital asset sector are formed from technology products. Vietnam is currently among the countries with a high level of participation in the digital economy and digital assets in Asia. It is estimated that approximately […]

The Vietnamese M&A market has just seen another deal significant enough to prompt investors and D2C founders to pause and analyze: Indian conglomerate Marico Limited spent approximately VND 750 billion to acquire 75% shares of Skinetiq, a company co-founded by Hannah Nguyen. If we deduce this, then […]

The collapse of JWR shows that not all platforms claiming to be "gold investments" are based on the same value foundation. When comparing JWR and HanaGold within the same frame of reference, the differences become clear, stemming from the nature of the product, the risk management mechanism, and so on.

The recent collapse of the JWR gold investment app in China has become one of the biggest shockwaves for the region's financial markets. With estimated losses exceeding 10 billion yuan, equivalent to approximately $1.4 billion, […]

In recent years, Real World Assets (RWA) has been seen as a new approach to applying technology to asset management, cash flow transparency, and optimizing capital connectivity. Globally, many independent studies have noted the growth rate […]

In the digital transformation of the financial and business markets, many organizations worldwide are seeking models that make physical assets transparent, easy to track, and convenient for governance and capital management. Among them, RWA (Real World Assets) stands out...

In the period 2024–2035, digitizing data related to assets, benefits and cash flows in a verifiable, automated and risk-controlled way is considered the direction many organizations in the world are researching. However, not all models “bring data […]

In the global capital market structure, the typical recurring cash flow asset group, bonds, is often considered the stable foundation of many portfolios. In Vietnam, after a period of rapid growth and then strong adjustment, the need for “transparency – standardization – number […]

Creative innovation is entering an era where the core value lies not only in the original work, but also in the exploitation rights that can be extended over time and space. From music, movies, fictional characters to images, designs, content […]